Goals of this article:

- Present existing GHG assessment standards and how a selection can be made

- Explain the common aspects of most GHG assessment standards

- Highlight how differences between standards might bring inconsistencies between studies

1. Selection of a GHG assessment standard

As mentioned in our blog article of July, many GHG assessment standards are now available to support organisations when they want to evaluate the impacts of their activities on climate and how they can set reduction targets. These standards have been defined by various international organisations like the ISO [1] or the GHG Protocol consortium [2] as well as governmental offices like the European Commission [3] or the US EPA [4]. They propose different accounting rules with diverse vocabularies to evaluate and disclose GHG emissions of various systems. Some standards use broad general rules that are deliberately designed in an open manner so that they may be applicable to most companies, products or services. Other standards are sector-, or even industry-specific, which means that they focus on rules for a limited part of the economy. The following web pages provide lists of existing GHG assessment standards.

- Wikipedia: Explanation of carbon accounting and existing standards

- Pre-Sustainability: Presentation of various standards and a strategy for their selection

- Plan A: Focus on GHG Protocol, with a presentation of other standards

Most standards have been focusing on direct and indirect energy-related GHG emissions (respectively scope 1 and 2), but there is a growing trend to include all the GHG emissions of the value chains (i.e. scope 3). The addition of scope 3 data means that standards are now effectively providing the guidelines to assess the full carbon footprint of organisations, products and services, which leads to more accounting efforts, but provides broader options to tackle climate change.

Many aspects can drive the selection of a GHG assessment standard by an organisation. Below you can find a list of key questions that should be answered when making such a choice.

- What is the system that will be analysed? A clear distinction can be made between standards that are proposed for corporations and standards that are proposed for products & services. It can also be important to consider the size of a company when answering this question since global corporations might have more complex value chains to consider than SMEs.

- In which sector of the economy is the analysed corporation, product or service? This will help in identifying the sector or industry-specific standards that could be of relevance.

- Are there national standards and legal disclosure requirements in the country of the organisation? The importance of this question is rather easy to understand, but the legislative landscape is evolving quickly and international corporations might have to deal with many standards.

- Is there a standard that includes most of the requirements of other standards? Selecting such a standard could simplify the adaptation of a GHG assessment to the context of other standards. This can be of particular relevance for corporations that need to share their evaluations with their customers and the general public.

- Is there a standard that has more recognition in the sector or country of the organisation? This is important to find a standard that will provide better brand recognition and facilitate the exchange of assessment between corporations (mainly for GHG assessment of products and services)

2. General procedure to carry out GHG assessments

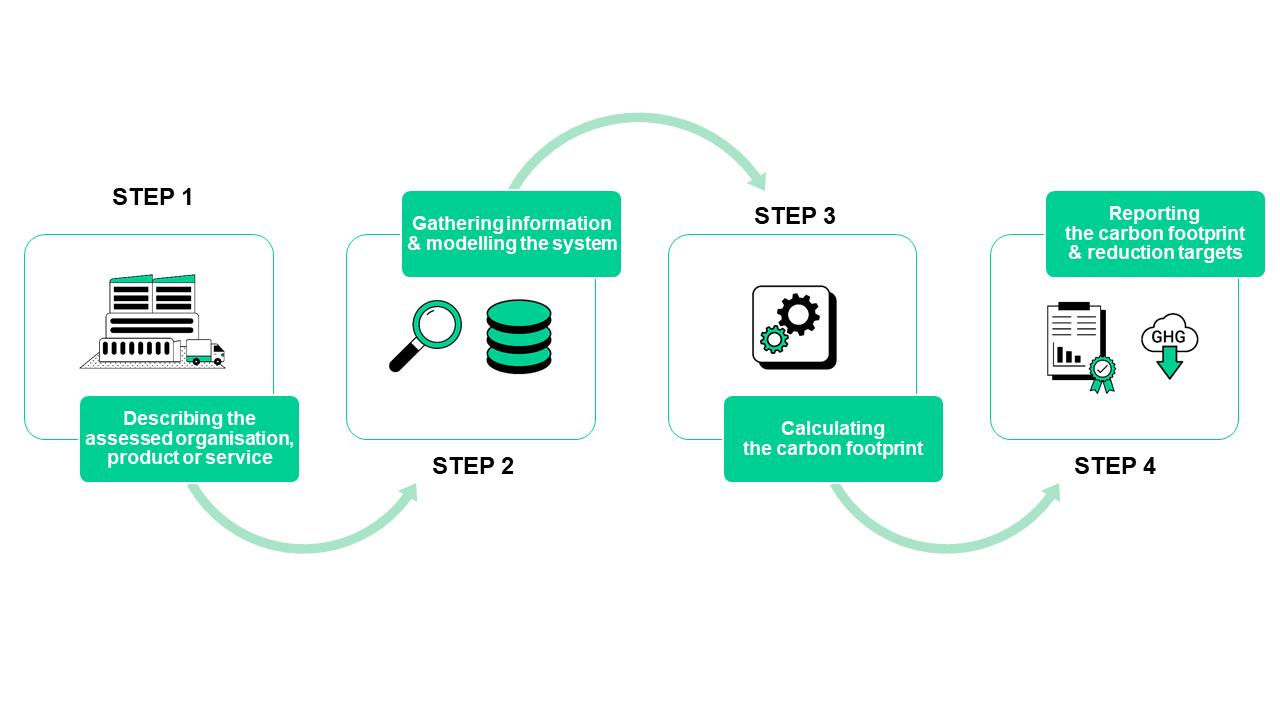

To ensure compliance, the first vital step is to familiarise yourself with the specific rules and guidelines of the chosen GHG reporting standard, but there is a common stepwise structure for most GHG assessment procedures. This structure has been clearly described by the Life Cycle Assessment (LCA) method, which is defined in the ISO 14000 series mainly with two documents that have been last updated in 2006 [5,6]. This common foundation is shown in the figure below.

The procedure to carry out most GHG assessments for both direct and indirect GHG emissions from organisations, products or services (i.e. scopes 1, 2 & 3) can be described by the four consecutive steps of the figure. The following paragraphs provide short descriptions of the steps.

Step 1: Describing the assessed organisation, product or service

This step, which is called “scope definition” in LCA standards [5,6], is critical for all assessments since it supports the transparent, consistent, and comprehensive description of analysed systems. It is a crucial aspect to define as it will serve as a future point of reference for fair comparisons between annual reports; or between the carbon footprints of various products and services..

In addition, all GHG assessment standards provide guidelines on the definition of system boundaries and modelling choices for the selected corporation, product or service (and their value chains if scope 3 is included). This guidance lists all the activities that need to be included or excluded from the assessment. They may also provide recommendations on which GHGs to consider as well as how carbon sequestration should be modelled. Instructions on more technical aspects like the model of electricity use and when the end-of-life of a value chain is reached are also defined here.

Aspects related to the representativeness of the models and considered data should also be informed in this step to provide an idea of how the results can be interpreted. This can be discussed in qualitative description of the time, place, and technology level of the considered activities. Each GHG assessment standard has its own recommendations and rules on this topic. The descriptions vary in their levels of detail but usually do not set specific requirements for what is considered representative.

Step 2: Gathering information and modelling the system

This step ensures that all relevant GHG emissions from various activities along the value chains can be modelled. It entails two types of information that are provided by different stakeholders.

Information from the organisation (foreground data – obtained from models and measurements)

This data should typically be sourced from internal records and measurements. It relates to the on-site activities, their GHG emissions, the amount of bought products and paid services (e.g. electricity) as well as the sold products and services if scope 3 data is to be included. A common challenge with this part of the assessment is the collection of data across different services since they often use different formats and types of files to store the information. Effective data management and integration practices are therefore essential to minimise efforts during this step.

Information from environmental databases (background data – obtained from models and statistics)

This data should normally come from external stakeholders like the US EPA [7] and the IPCC [8] that provide GHG emission factors (EFs) for energy-related activities (i.e. scope 2) or for complete value chains (i.e. scope 3). The ecoinvent association is another example of a data provider that specialises in full LCA datasets, which also offer scope 3 GHG EFs. Using such data can be challenging when:

- Connecting the GHG EFs of products and services from the environmental database to the specific names of products & services that are bought by the organisation under assessment.

- Checking that the provided GHG EFs are consistent with the rules and requirements of the selected standards (this is not currently verified unless experts are involved).

Step 3: Calculating the carbon footprint (when scope 3 data is included)

This step is rather straightforward when all the data has been gathered. It involved the multiplication of organisational data (foreground) with their related GHG EFs (background) and the aggregation (i.e. addition) of complete GHG emissions from different activities. The aggregation will be done by following the rules and guidelines of selected standards (see also reporting) and will often be provided in amounts of CO2-eq. values to consider all GHG emission with a common basis [9]. Different digital solutions can be used for this step ranging from Excel tables to fully integrated solutions like the Microsoft Sustainability Manager or the Pelt8 Platform.

Step 4: Reporting the carbon footprint and reduction targets

The reporting is a crucial result of any GHG assessment, not only for internal management purposes but also to meet the new political regulations as well as the needs of customers for clear and trustworthy scope 3 data. Different standards will have different requirements and vocabularies for this step, but they will always ask to inform on key choices that were made in the previous 3 steps. First and foremost, it is expected that all reports be clear, transparent, and compliant with the chosen GHG assessment standard. This involves a presentation of the total carbon footprint, a description of GHG by sources and by types of activities as well as insights into potential reduction strategies. There are other, more detailed elements which list all the qualitative discussion on the representativeness of the assessment in relation to what has been considered and the limitations of the assessment.

3. The differences that matter

The previous section shows that there is a clear common structure to all GHG assessment standards and how evaluations should typically proceed. With that being said, the devil is in the details and the differences between standards prevent simple and consistent comparisons between assessments, which means that exchange of GHG knowledge between organisations is currently very challenging. Here are some examples of aspects that impede consistent comparison.

Differences in system boundaries: If two organisations or value chains do not consider activities at the same level of comprehensiveness, there is a high probability that some GHG sources will be neglected in one of the assessments. This means that comparisons between assessments will not be made on equal grounds. This can happen if the standards are forcing different limits like considering more or less types of GHG emissions. It might also be explained by the use of different environmental databases that have different levels of comprehensiveness.

Differences in how a system is modelled: The web of human activities around the world is complex and it is possible to model it in many ways. For instance, it is reasonable to consider that a company is using the electricity that is physically provided in the region of its activities, which leads to a specific representation of related GHG emissions. On the other hand, it is also reasonable to link the electricity use of a company to the energy sources that they pay for, which may lead to a completely different picture if substantial amounts of renewable energy are bought with certificates. Both options have their merits and are accepted in assessment standards, but they should not be used at the same time.

Differences in the background data sources: Database providers can use different sources of information to evaluate the scope 3 GHG emissions of various activities. These sources of information can be more or less detailed, follow different modelling choices and may be updated at different times. Furthermore, the database providers have to use complex models that are rarely described in all their details, which prevent any consistency checks between background databases. For all these reasons, it is difficult to check if two assessments that use different background databases are actually comparable even if a selected standard allows this.

Differences in the formats and vocabularies: The many organisations behind the various existing standards are connected to different regions of the world and sectors of the economy, which makes it easy to understand why they use different formats and naming conventions for their disclosure requirements. While easily understandable and very difficult to change, this nevertheless hinders clear and efficient comparison between assessments because the translation or aggregation of results in different formats requires the support of experts even if all other aspects are consistent.

With all this in mind, it becomes clear that organisations that have a detailed understanding of the different rules from diverse GHG assessment standards will be the only ones that may consistently consider the carbon footprints of their suppliers when assessments are made with different standards.

Stay tuned for our upcoming article where we aim to address the topic of scope 3 data!